As the new year approaches, businesses of all sizes have the opportunity to reassess their financial strategies and implement tax planning techniques that optimize operations and minimize tax liabilities. Effective tax planning is crucial for ensuring compliance with tax laws and regulations while maximizing savings and improving the bottom line. This comprehensive guide explores various tax planning strategies businesses can employ to achieve financial efficiency and long-term success.

Understanding the Importance of Tax Planning

Tax planning is a proactive approach to managing a business’s tax obligations. By carefully analyzing a company’s financial situation, tax planning allows business owners and managers to identify legal methods to minimize tax liabilities. Effective tax planning strategies involve making informed decisions and taking advantage of available deductions, credits, exemptions, and incentives provided by tax laws and regulations. The primary goal of tax planning is to optimize a business’s tax position while ensuring compliance.

Key Tax Planning Strategies:

Timing and Shifting Income and Expenses

One of the most effective tax planning strategies is timing and shifting income and expenses. By strategically timing the recognition of income and shifting expenses, businesses can optimize their taxable earnings and potentially reduce their overall tax liability. Here are some key considerations:

Income Deferral: Deferring taxable income to the following tax year can help reduce the current year’s tax burden. Consider delaying the completion of projects or postponing the issuance of invoices until the new year to defer income recognition.

Expense Acceleration: Accelerating deductible expenses can significantly lower taxable income for cash basis taxpayers. This includes prepaying expenses such as rent, insurance premiums, or office supplies before the year-end. For those on an accrual basis, it is advisable to review expenses and accrue what is applicable. For example, wages that are paid in January for work performed at the end of December can be accrued and deducted in December, before actual payment. This approach can also apply to other expenses like utilities, contractor payments, and certain taxes.

Maximizing Business Tax Deductions

Taking advantage of available business tax deductions is another crucial tax planning strategy. By carefully analyzing eligible expenses, businesses can reduce their taxable income and minimize their overall tax burden. Here are some common deductions to consider:

Operating Expenses: Deductible business expenses include rent, utilities, office supplies, professional services fees, advertising costs, and insurance premiums. Keeping detailed records of these expenses is essential to support deductions.

Employee Benefit Programs: Contributions to health insurance premiums, health savings accounts (HSAs), flexible spending accounts (FSAs), and other qualified employee benefit programs are deductible expenses that can benefit both employees and the business.

Retirement Plans: Establishing tax-advantaged retirement plans, such as a 401(k) or SEP IRA, not only helps with retirement savings but also provides tax deductions on contributions.

Business Travel and Meals: Expenses related to business travel, including transportation, lodging, and meals, can be deductible. Proper documentation is crucial to support these deductions.

Maximizing Tax Credits and Incentives

Identifying and utilizing tax credits and incentives can provide significant tax advantages for your business. By leveraging government credits and incentives, businesses can further reduce their tax liabilities. Here are some tax credits and incentives to consider:

Research and Development (R&D) Tax Credits: If your business invests in qualifying research and development activities, you may be eligible for R&D tax credits. These credits can help offset the costs associated with innovation and product development.

Energy-Efficient Upgrades: Businesses that invest in energy-efficient upgrades, such as solar panels or energy-saving equipment, may qualify for tax credits or incentives at the federal or state level.

Work Opportunity Tax Credit (WOTC): The WOTC provides tax credits to businesses that hire individuals from certain target groups, such as veterans, ex-felons, or individuals receiving government assistance.

State and Local Incentives: Many states offer tax incentives and credits to businesses that create jobs, invest in certain industries, or contribute to economic development. Research and explore incentives specific to your location.

Choosing the Right Business Systems

Implementing efficient business systems is crucial for streamlining operations and ensuring accurate financial reporting. When selecting new accounting, inventory, and payroll systems, several factors should be considered:

Integration and Scalability: Evaluate how well the system integrates with existing operations and whether it can scale with business growth.

Compliance and Security: Ensure that the system meets regulatory requirements, such as data privacy and security measures, to protect sensitive business and customer information.

Cost-Benefit Analysis: Consider the return on investment (ROI) of implementing a new system compared to the cost of continuing with the current one. Evaluate the long-term benefits and potential cost savings.

User Experience and Support: Assess the system’s user-friendliness and the level of customer support available. A user-friendly system with responsive support can enhance operational efficiency.

End-of-Year Tax Mitigation Strategies

As the year-end approaches, businesses can implement various strategies to reduce their tax burdens. Here are some end-of-year tax mitigation strategies to consider:

Equipment and Asset Purchases: If your business needs new equipment or assets, consider making the purchase before year-end to take advantage of depreciation deductions or applicable tax incentives.

Bad Debt Write-Offs: Review your accounts receivable and identify any uncollectible debts. Writing off bad debts can reduce your taxable income for the current year.

Charitable Contributions: Donate to qualified charitable organizations and take advantage of tax deductions for your contributions. Ensure that the organization is eligible for tax-deductible donations.

Retirement Plan Contributions: Maximize contributions to retirement plans, such as a 401(k) or SEP IRA, before year-end to benefit from tax deductions and reduce taxable income.

Understanding and Implementing Section 471(c)

Section 471(c) of the Tax Cuts and Jobs Act (TCJA) offers a strategic opportunity for certain businesses, particularly cannabis businesses, to potentially mitigate the impact of 280E and reduce their taxable income. While this may seem similar to the cash method of accounting, it is crucial for businesses to understand that Section 471(c) is distinct and requires a careful analysis to ensure compliance with its specific regulations and to fully benefit from its potential tax advantages.

Implementing Section 471(c) requires a thorough understanding of inventory accounting methods, potential tax savings, and compliance considerations. Consult with a qualified tax professional to determine if implementing Section 471(c) is suitable for your business and to ensure compliance with tax laws.

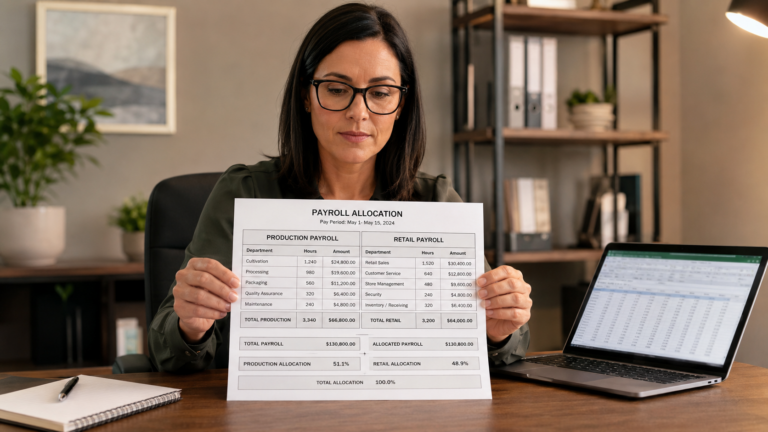

Payroll Solutions and Tax Compliance

Proper payroll management is essential for tax compliance and minimizing errors. Here are some considerations for choosing the right payroll system and ensuring tax compliance:

Automation and Accuracy: Choose a payroll system that automates payroll calculations and ensures accurate tax withholding, including federal, state, and local taxes.

Tax Filing and Reporting: Verify that the payroll system can generate required tax forms, such as W-2s and 1099s, and file them timely with tax authorities.

Employee Benefits and Retirement Contributions: Ensure that the payroll system can handle employee benefit deductions, retirement plan contributions, and other payroll-related tax considerations.

Tax Withholding Calculations: The payroll system should accurately calculate employee tax withholdings based on the employee’s filing status, exemptions, and other relevant factors.

Year-End Accounting and Financial Compliance

Year-end accounting is crucial for accurately reporting financial information and ensuring compliance with tax laws. Consider the following steps for year-end accounting:

Reconcile Accounts: Perform a thorough reconciliation of all financial accounts, including bank accounts, credit card statements, and vendor invoices. This helps identify any discrepancies and ensures accurate financial reporting.

Review Financial Statements: Analyze financial statements, including balance sheets, income statements, and cash flow statements, to assess the business’s financial health and identify areas for improvement.

Prepare for Audits: If your business is subject to audits, ensure that you have all necessary documentation and records readily available. This includes supporting documents for deductions, credits, and other financial transactions.

Comply with Regulatory Deadlines: Stay informed about tax filing deadlines and comply with all applicable regulations to avoid penalties or interest charges.

Conclusion

Effective tax planning is a key component of running a successful business. By implementing tax planning strategies, businesses can optimize their operations, minimize tax liabilities, and maximize savings. From timing income and expenses to maximizing deductions and utilizing tax credits, small businesses have numerous opportunities to enhance their financial efficiency and compliance. However, tax planning can be complex, and it is essential to consult with qualified professionals to ensure proper implementation and compliance.

At GreenGrowthCPAs, we understand the unique challenges faced by businesses in various industries, especially at this time of the year. Our team of experienced CPAs and tax professionals can provide comprehensive tax planning services tailored to your specific needs. Whether it’s optimizing tax strategies, implementing Section 471(c), or choosing the right payroll system, we are here to help you navigate the complexities of tax planning and ensure compliance with tax laws. Contact us today to learn how we can assist you in achieving financial efficiency and long-term success.